RETIREMENT ANNUITIES ? ANY GOOD?

By Warren Ingram

JOHANNESBURG: It is almost unknown for a financial planner in South Africa to deride Retirement Annuities (RA's) even though insurance agents have used them to swindle investors for many decades. So, any article about RA's is likely to draw criticism based on valid past experience even if the products themselves have changed. This article is an attempt to provide a balanced view of RA's as they are an important part of the personal finance landscape in SA. I was sent an email asking whether people should invest on their own or via retirement funds/RA's and decided to write this article in reply. I asked Daniel R Wessels who is the editor of www.indexinvestor.co.za to run a model for me to see what the numbers tell us about RA's. Wessels does some great research on the benefits of index investing and provides much of this information on his website.

THE QUESTION

This is the question that was sent to me by Craig, "A friend and I were debating the merits of two investment approaches and in the end we could not agree on which actually was the best way of going about investing. Essentially the one approach is to invest on your own and the other is to invest in a unit trust via a pension/provident fund."

THE ANSWER

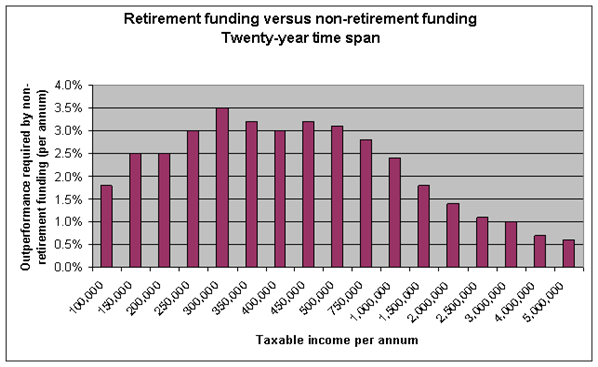

In short, the numbers definitely favour RA's in almost all situations. The graph below was provided by Wessels and shows the amount of additional growth needed per year for your own portfolio to overcome the tax benefits provided by an RA.As Wessels says, "From my analysis it was clear that in most cases and at different taxable income levels an individual would be better off making use of an approved RA structure (i.e. tax deductibility benefits) versus trying to build your retirement wealth with after-tax monies."

The graph above assumes that you get the identical growth from your own portfolio and the RA. In addition, it assumes that all other aspects such as costs are the same. If you earn R300,000 per year and you invest in your own portfolio, it will need to grow by 3.5% per year more than an RA investment. This is a very difficult benchmark to beat, especially with the advent of modern unit trust-based RA's. If you add costs into the equation, it is likely that your own portfolio will be cheaper than an RA however, it is possible to get very low cost RA's that invest in unit trusts. Some companies even offer the RA for free provided you invest in their unit trusts. I also understand from Mike Brown of www.etfsa.co.za that he is working on RA's that invest in Exchange Traded Funds (ETF).

THE SAD HISTORY OF RA'S

In the past, assurance companies sold very expensive RA's that paid insurance agents massive upfront commissions and delivered very poor growth to investors. The actual investment portfolios were so opaque and the investment reporting was so poor that you had no idea what was actually happening to your money.The whole situation was made worse because you could not move your RA to another company or cancel the investment without paying even more costs. With the advent of the unit trust industry, new product providers have starting offering low cost RA's that invest exclusively in unit trusts. The reporting is much more transparent and the costs have reduced substantially so that you can now get an RA for a total cost of 1.75% per year. In addition, the laws around these products have changed which means you can now move your RA (with a bit of difficulty) between product providers. As a result, you can now derive the full tax benefits of RA's without having to pay massive costs and the costs can be paid on a pay-as-you-go basis i.e. not upfront.

ANY DOWNSIDES TO RA'S?

Once you start a retirement annuity, you cannot access your capital until you are 55 years old. At that time, you will be able to get a lump sum with a portion of your capital whilst the balance will need to be invested - preferably in a unit-trust based living annuity. You can draw a monthly income from the living annuity until the money is depleted or you can leave it to your beneficiaries in the event of your death. If you have financial problems, you cannot access the money in your RA until you are 55 years old. The upside is that your creditors also cannot access this money. In addition, you cannot transfer your retirement annuity or living annuity to an offshore retirement fund if you emigrate. You will only be able to move the income from the living annuity after you turn 55 but not the capital.

CONCLUSION

I believe RA's have an important role to play in any working personal financial planning. With all the new legislation and transparency offered by unit trust based RA's I have little fear of recommending them to investors. Unfortunately, the old fashioned (bad) RA's still exist and these are not good investments. My recommendation is to invest in products offered by specialist investment companies and avoid paying upfront fees.